U.S. Beef, Veal, Lamb And Mutton Market. Analysis And Forecast to 2030

Get instant access to more than 2 million reports, dashboards, and datasets on the IndexBox Platform.

View PricingBeef Market - U.S. Beef, Veal, Lamb and Mutton Supplies to Japan and South Korea are Expected to Increase

From 2008 to 2015, the U.S. beef market showed negative dynamics, falling from X million pounds to X million pounds. Although consumption decreased, overall market value increased thanks to more value-added products being launched on the market. Following gradual price increases, market revenue consistently grew. In value terms, the U.S. beef, veal, lamb and mutton market was estimated at X billion USD in 2015, growing by +X% annually between 2008 and 2015. A significant drop was observed last year, when the market value decreased by X% due to a record fall in prices.

U.S. growth in red meat consumption is expected to accelerate to +X% (currently -X%) in the medium term, amid the current economic recovery and a growing demand for high-end fresh meat cuts and upscale meat products.

U.S. red meat manufacturing illustrated negative dynamics, decreasing from X million pounds in 2008 to X million pounds in 2015. The CAGR dropped -X% over the period under review. In value terms, U.S. beef, veal, lamb and mutton production posted solid gains since 2010, only to fall by X% in 2015, finally reaching X billion USD.

U.S. producers benefited from expanding meat exports, which accounted for a X% share in U.S. manufacturing. U.S. companies are well-known suppliers of high-quality grain-fed beef. In 2014, the main destinations of U.S. beef, veal, lamb and mutton exports were Mexico (X%) and Japan (X%), followed by the Republic of Korea (X%), Canada (X%) and China (X%). These five leaders together comprised X% of U.S. exports. The share exported to Mexico increased (+X percentage points), while the share sent to Japan (-X percentage points) and Canada (-X percentage points) illustrated negative dynamics. U.S. beef supplies to Japan and South Korea are projected to increase, due to the recovery of these markets, which were closed to the United States following the first U.S. case of bovine spongiform encephalopathy (BSE) in December 2003.

It is expected that U.S pork exports will continue an upward trend in the mid-term, fueled by growing production efficiency. U.S. producers will strengthen their positions on export markets, particularly in Pacific Rim nations and Mexico. The Russian market will be closed for U.S. exports into the near future as a result of sanctions against the country, as well as rapidly increasing domestic production there.

Imports should not be regarded as strong factors influencing U.S. market dynamics in the medium term. Canada and Australia were the main suppliers of beef, veal, lamb and mutton into the U.S., with a combined share of X% of total U.S. imports in 2014. However, the fastest growing supplier was Mexico (+X% per year). This country strengthened its position in the U.S. import structure, from X% in 2007 to X% in 2014. By contrast, Canada saw its share reduced to X%.

The U.S. is projected to keep its dominance in global imports of beef, primarily of grass-fed, lean beef from Australia, New Zealand, and NAFTA countries, for use in ground beef and processed products.

Net US exports of beef, veal, lamb and mutton has shown a positive trend since 2007. In 2014 this industry ran a significant trade surplus of X million USD, approximately X% of gross exports. This surplus could grow substantially in the years to come.

Do you want to know more about the U.S. beef market? Get the latest trends and insight from our report. It includes a wide range of statistics on

- beef market share

- beef prices

- beef industry

- beef sales

- beef market forecast

- beef price forecast

- key beef producers

Join Us at HANNOVER MESSE 2024

Don’t miss your chance to connect with us directly. Schedule a personal meeting to dive deeper into how solutions.

Hall 002, Stand C10. 22 - 26 April 2024 | Hannover, Germany

This report provides an in-depth analysis of the beef market in the U.S.. Within it, you will discover the latest data on market trends and opportunities by country, consumption, production and price developments, as well as the global trade (imports and exports). The forecast exhibits the market prospects through 2030.

Product coverage:

- NAICS 311611 - Animal (except poultry) slaughtering

Companies mentioned:

- Tyson Foods

- Hormel Foods Corporation

- Seaboard Corporation

- Smithfield Foods, Morrell John & Co

- Clemens Food Group

- Amick Farms

- National Beef Packing Company

- FPL Food

- Indiana Packers Corporation

- Dietz & Watson

- Smithfield Farmland Corp.

- Transhumance Holding

- Triumph Foods

- Sam Kane Beef Processors

- Rosen's Diversified

- American Foods Group

- The Smithfield Packing Company Incorporated

- Plumrose USA

- Cargill Meat Solutions Corp

- Buckhead Beef Company

- Emmpak Foods

- Nebraska Beef

- American Beef Packers

- Jbs Usa

- Pinnacle Foods

- Tyson Fresh Meats

- Green Bay Dressed Beef

- Jbs USA Holdings

- Half Moon Deer Processing

Country coverage:

- United States

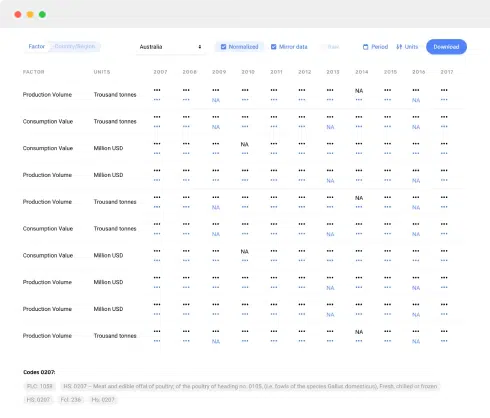

Data coverage:

- Market volume and value

- Per Capita consumption

- Forecast of the market dynamics in the medium term

- Trade (exports and imports) in the U.S.

- Export and import prices

- Market trends, drivers and restraints

- Key market players and their profiles

Reasons to buy this report:

- Take advantage of the latest data

- Find deeper insights into current market developments

- Discover vital success factors affecting the market

This report is designed for manufacturers, distributors, importers, and wholesalers, as well as for investors, consultants and advisors.

In this report, you can find information that helps you to make informed decisions on the following issues:

- How to diversify your business and benefit from new market opportunities

- How to load your idle production capacity

- How to boost your sales on overseas markets

- How to increase your profit margins

- How to make your supply chain more sustainable

- How to reduce your production and supply chain costs

- How to outsource production to other countries

- How to prepare your business for global expansion

While doing this research, we combine the accumulated expertise of our analysts and the capabilities of artificial intelligence. The AI-based platform, developed by our data scientists, constitutes the key working tool for business analysts, empowering them to discover deep insights and ideas from the marketing data.

-

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

-

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDS This Chapter is Available Only for the Professional Edition PRO

-

3. MARKET OVERVIEW

Understanding the Current State of The Market and Its Prospects

- MARKET SIZE

- MARKET STRUCTURE

- TRADE BALANCE

- PER CAPITA CONSUMPTION

- MARKET FORECAST TO 2030

-

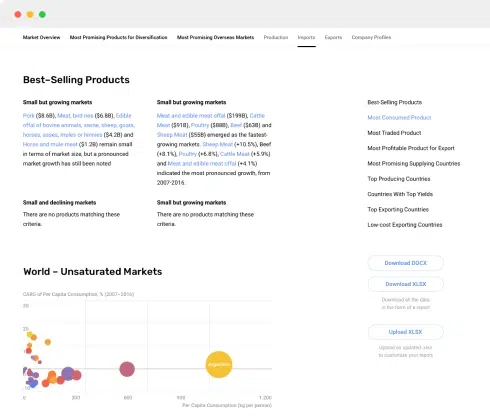

4. MOST PROMISING PRODUCT

Finding New Products to Diversify Your Business

This Chapter is Available Only for the Professional Edition PRO- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCT

- MOST TRADED PRODUCT

- MOST PROFITABLE PRODUCT FOR EXPORT

-

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

This Chapter is Available Only for the Professional Edition PRO- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

-

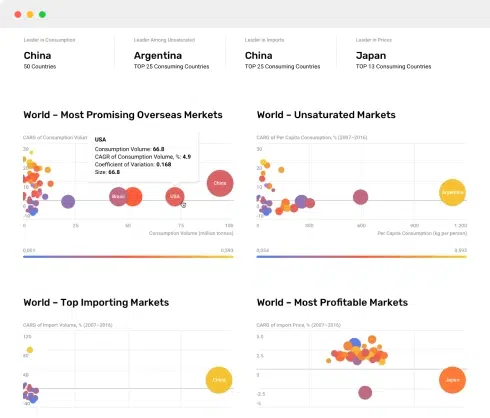

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Exports

This Chapter is Available Only for the Professional Edition PRO- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS FROM 2012–2023

- IMPORTS BY COUNTRY

- IMPORT PRICES BY COUNTRY

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS FROM 2012–2023

- EXPORTS BY COUNTRY

- EXPORT PRICES BY COUNTRY

-

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

This Chapter is Available Only for the Professional Edition PRO -

LIST OF TABLES

- Key Findings In 2023

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Per Capita Consumption In 2012-2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023

-

LIST OF FIGURES

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Market Structure – Domestic Supply vs. Imports, In Physical Terms, 2012-2023

- Market Structure – Domestic Supply vs. Imports, In Value Terms, 2012-2023

- Trade Balance, In Physical Terms, 2012-2023

- Trade Balance, In Value Terms, 2012-2023

- Per Capita Consumption, 2012-2023

- Market Volume Forecast to 2030

- Market Value Forecast to 2030

- Products: Market Size And Growth, By Type

- Products: Average Per Capita Consumption, By Type

- Products: Exports And Growth, By Type

- Products: Export Prices And Growth, By Type

- Production Volume And Growth

- Exports And Growth

- Export Prices And Growth

- Market Size And Growth

- Per Capita Consumption

- Imports And Growth

- Import Prices

- Production, In Physical Terms, 2012–2023

- Production, In Value Terms, 2012–2023

- Imports, In Physical Terms, 2012–2023

- Imports, In Value Terms, 2012–2023

- Imports, In Physical Terms, By Country, 2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, 2012–2023

- Exports, In Value Terms, 2012–2023

- Exports, In Physical Terms, By Country, 2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023